Residential Fire Damage Claims

Fire damage claims require careful attention to detail, as they often involve extensive property loss. We guide homeowners through the claims process and ensure they receive all they are entitled to under their policy.

We help families navigate complex home insurance claims so they can focus on what matters most.

A house fire or flood can be unexpected, fast, and devastating, leading to significant loss for your family. At Virani Law, we have experienced and navigated the exact challenges you face during these trying times. Our dedicated Recovery Process is designed to guide you through every step, ensuring you receive the support and compensation you need to rebuild your life and restore your home.

“After being told there was no compensation available, we felt completely stuck. Virani Law took the time to truly understand our situation and advocate for our family. Their support made all the difference in helping us move forward.”

The Beauchesne Family

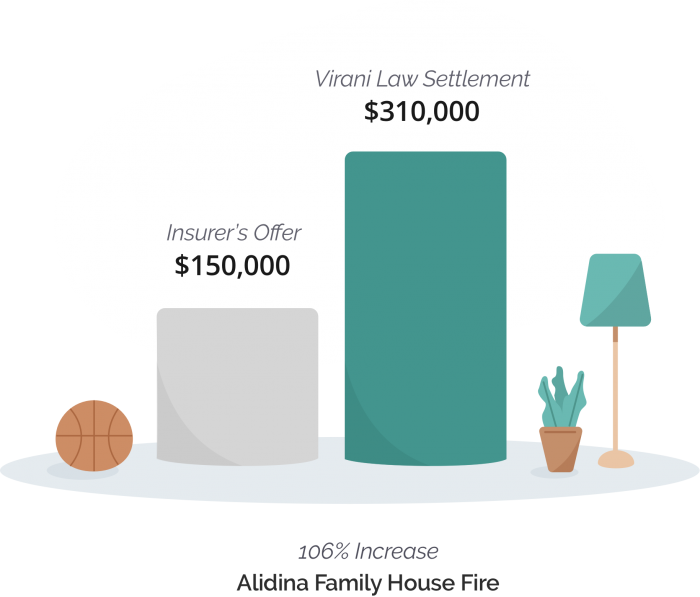

Virani Law secured a six-figure settlement for the Family who had been offered no compensation after the Fort McMurray wildfires.

Insurance claims can be complex and emotionally draining. What sets Virani Law apart is not just legal expertise, but a commitment to guiding homeowners with care, clarity, and strong advocacy when it matters most.

Clear guidance through complex insurance policies

Thorough, accurate documentation that protects your claim

Strong advocacy for fair compensation

Support that extends beyond the legal process

We are a dedicated team of lawyers, paralegals, and legal support staff with over 10 years of experience in insurance claims related to residential property damage caused by natural disasters. We’ve successfully represented clients across Canada in the aftermath of devastating losses.

Fire damage claims require careful attention to detail, as they often involve extensive property loss. We guide homeowners through the claims process and ensure they receive all they are entitled to under their policy.

Residential flood damage claims can be complex due to the varying types of water damage and the specific coverage details outlined in insurance policies. We help homeowners navigate this intricate process.

After experiencing damage to your home, the first step is to ensure your safety and the safety of others. Once it is safe to return:

Report the incident promptly.

Contact your insurance company as soon as possible to initiate the claims process. Most insurance policies require you to file a claim within a specific timeframe, often within days of the incident.

Understand the next steps.

After reporting the damage, your insurance company will assign an adjuster to assess the damage and begin evaluating your claim.

Document all damage thoroughly.

Take pictures and videos and create a detailed list of affected items. This can significantly impact the outcome of your settlement.

Stay organized and communicate clearly.

Be prepared to provide any requested documentation and maintain open communication with your insurer throughout the process. Staying organized and proactive can reduce delays and support a smoother claims process.

Damage to your home results in three distinct coverage areas. Compensation varies from policy to policy.

Covers the cost to repair or rebuild your home after damage.

Common Issues

Covers repair or replacement of damaged personal belongings.

Common Issues

Covers temporary living costs if you can’t stay in your home.

Common Issues

Navigating residential damage insurance claims can be challenging. These claims often involve strict deadlines, complex policy language, and disputes over coverage or valuation. A residential damage lawyer is essential in protecting your rights from the very beginning. They will review your policy, identify any coverage gaps, and manage communications with your insurer on your behalf. For homeowners across Canada, involving a lawyer early can help prevent delays, low settlement offers, or denied claims due to exclusions or documentation issues. Your lawyer will also handle evidence collection, expert reports, and negotiations, significantly reducing your stress while keeping your claim on track.

No, hiring a residential damage lawyer typically helps move your claim forward more efficiently. A lawyer ensures that all insurer requirements are met, deadlines are respected, and documentation is submitted correctly the first time. Delays often occur when insurers request additional information, dispute compliance, or question how the damage happened. With legal guidance, these issues can be addressed proactively, keeping communication focused and well-documented. By preventing missteps that could trigger reviews or denials, a lawyer can help you reach a fair settlement faster, avoiding a prolonged back-and-forth with the insurer.

What sets us apart is our unique combination of legal expertise and personal experience. Founded by Fy Virani, who has firsthand experience with a devastating house fire, we take a deeply client-focused approach. Our clients are supported through a structured Recovery Process that includes policy review, damage documentation, access to free counselling sessions with a therapist, and negotiations with insurers. Our firm emphasizes clear communication, personalized claim strategies, and access to additional support resources when needed. This holistic approach, available across Canada, allows our clients to pursue fair compensation while focusing on their recovery, rather than getting bogged down in insurance disputes.

After residential property damage, these are the four steps that should be taken:

Residential property damage claims typically arise from sudden or catastrophic events that render a home unsafe or uninhabitable. Common types of claims include:

Additionally, some claims may involve secondary damage, such as smoke contamination, mould growth, or structural issues that develop after the initial loss.

Navigating the claims process can be challenging for policyholders. A public adjuster is hired by the policyholder to inspect damage, prepare estimates, and negotiate with the insurance company. Their primary focus is on assessing and valuing the loss. However, it’s important to note that public adjusters cannot provide legal advice, interpret policy disputes, or challenge insurer decisions using legal tools. When coverage is denied, delayed, or undervalued, an insurance lawyer is better equipped to address contractual issues, enforce policy rights, and escalate disputes when negotiations stall.

You can contact Virani Law by phone or through our website to request a consultation. Our team is dedicated to working with homeowners across Canada, providing guidance at any stage of the claims process. Whether you are just starting a claim or facing delays, denials, or settlement disputes, reaching out early allows us to assess your situation and clarify the next steps with confidence. Don’t hesitate to contact us for the support you need.

Most home insurance policies require you to report damage within a specific timeframe, typically between 30 to 90 days. However, it’s essential to check your policy for exact deadlines, as failing to report within this period may affect your eligibility for compensation.

Whether to claim for minor damage depends on the cost of repairs and your deductible. If the repair costs are close to or less than your deductible, it may not be worth filing a claim, as it could impact your premiums.

Home insurance typically does not cover damage from natural disasters like floods or earthquakes unless you have specific endorsements. Other exclusions may include wear and tear, neglect, and damage from pests. Always review your policy for detailed exclusions.

At Virani Law, we are dedicated to helping homeowners recover, resolve, and rebuild by ensuring you receive the compensation you deserve for your residential damage claim.

Schedule a time for us to give you a call so that we can better understand what you are going through.

For any questions feel free to call us at (519) 515-0010