What Are Business Contents?

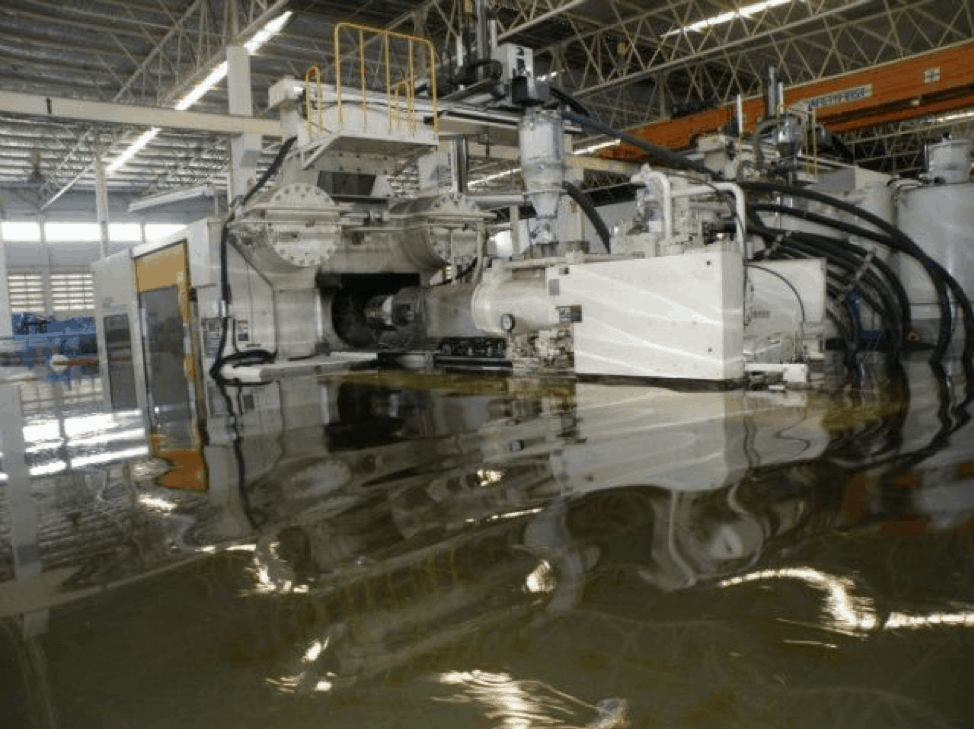

A flood has impacted your business and affected everything in it. Whether it was caused by a sewage backup or flood water coming in from the outdoors, water damage can be expensive to clean up. Not only will your business be affected for weeks or even months, but you will have to replace everything that has been damaged by the flood.

Business contents insurance will help you replace the items you have lost, but first, you should understand how the different types of items in your business are categorized and how that will affect your insurance claim. There are three general types of items at a place business: inventory, equipment, and business contents.

Understanding the difference between the three will help you deal with the flood damage and file an insurance claim.

#1 What Is Inventory?

Inventory is the merchandise or goods a business sells, either at the retail level or to another business further down the supply chain. These are goods and materials intended for resale to generate revenue for your business. Your business may be responsible for the manufacture, transportation, or final sale of these items at the retail level.

Importantly, your inventory does not include equipment, supplies, or business contents. Distinguishing between inventory and supplies is important for businesses that keep track of the difference between overhead costs and direct production costs. These are expressed as fixed and variable expenses. Fixed expenses include the purchase of supplies – the actual costs may vary, but there is a correlation between these costs and a business’s output. Higher output equals higher fixed costs. Variable costs do not always show this same correlation. They include inventory and payroll. These are the costs of conducting business, whether it’s in manufacturing, retail, service and hospitality, or professional services like the medical industry.

One important reason for the separate definition of inventory is that you typically have not paid sales tax on inventory. Sales tax is typically only applied once, at the retail level. In the case of contents such as supplies like stationary, your business is the final consumer and pays sales tax on those items. With inventory, you are selling them to another customer, whether it’s at the retail stage or you are part of the supply chain. The sales tax status of inventory affects their replacement value when it comes to your insurance.

#2 What Is Equipment?

Equipment is part of your business’s fixed assets. This includes all machinery, containers, vessels, tools, fixtures, and other apparatus used in your establishment. Manufacturers will have some of the most expensive equipment, but they are not the only businesses that will have it. Any business can have equipment if it is an asset held in the long-term and used to produce, sell, store, ship, or provide goods and services.

If you’re not sure if an item affected by flooding should be considered equipment, find out if you deduct its depreciation from your taxes. There is a good chance that the item in question is considered equipment if you do.

It is important to note that electronics may not be considered equipment for insurance purposes. Items like computers, laptops, mobile phones, and other electronics may be considered business contents.

#3 What Are Business Contents?

Business contents cover a range of items not covered under equipment or inventory. Whether your business is an office, a factory, a retail store, or a restaurant, your business contents will be worth a considerable amount of money. Here are some of the items that could be considered business contents:

- Laptops & smartphones

- Point of Sales terminals

- Printers and photocopiers

- Desks, chairs, and other office furniture

- Restaurant tables, chairs, and bars

These items can be insured either at actual cash value or replacement costs. Replacement cost coverage means the insurer will provide you with funds to replace your business contents with the same or similar items at their present-day price. Actual cost value coverage means that the insurer will pay the present-day value of your specific business contents, accounting for depreciation. It is important to know which kind of coverage you have, as the size of your reimbursement can differ considerably.

Supplies are generally considered business contents. Supplies can include everything from paper clips to printer ink to computing and printing systems. Supplies are just as essential to running your business like equipment, but are considered under a different category for tax deductions and should be listed separately in your insurance claim.

It can help to consider how long you expect to use supplies vs. equipment. While equipment is usually intended for long-term use, supplies are short-term. Whereas equipment depreciates on your balance sheets, supplies would be expensed.

It is also important to note that supplies are purchased for business purposes only, not for personal use. Personal items belonging to the business owners or employees may not be covered under business insurance.

Business Contents vs. Business Interruption Insurance

Business contents coverage is typically part of a broader business policy of insurance, which may also encompass business interruption insurance. Business interruption insurance covers:

- Lost revenue during your period of rebuild and recovery, and potentially supplemental revenue while your business gets back on its feet if you have extended coverage

- Revenue lost due to a property loss affecting your suppliers, customers, or a leader property

- Ordinary business expenses which continue during the period of rebuild and recovery

Another section of your business insurance policy covers the repair and rebuilding costs to the structure of your business.

If you are uncertain about how to navigate your business insurance claim after a flood or fire, we’re here to help businesses and individuals affected by flooding. Explore our website to find more resources on business insurance and the steps you can take to make sure your business gets back on its feet. Talk to your accountant about calculating expenses and create a business plan for getting your operations back to normal. Your business insurance policy can help you rebuild your business and replace valuable contents, equipment, and inventory.